“Fake Chinese Income” Mortgages Fuel Toronto Real Estate Bubble: HSBC Bank Leaks

The whistleblower, a Canadian business school graduate, was staggered by the suspicious home loans he discovered in 2022 when he joined a mortgage approval team in a small HSBC branch on the outskirts of Toronto.

He knew of suspicions surrounding Chinese capital in British Columbia real estate, but had never witnessed shady lending while working at an HSBC branch in Campbell River, a bucolic town on the coast of Vancouver Island.

When he arrived at HSBC’s bank in Aurora, an affluent suburb north of Toronto, he discovered explosive growth in home loans to Chinese diaspora buyers during the Covid-19 pandemic.

Chinese migrants living across Toronto were obtaining mortgages from HSBC while supposedly earning extravagant salaries from remote-work jobs in China. In one example, an Ontario casino worker that owned three homes also claimed to earn $345,000 in 2020 analyzing data remotely for a Beijing company.

Before joining HSBC Canada, the whistleblower had studied fake-income mortgage frauds for his Business Masters degree at Vancouver Island University. After arriving at Aurora in February 2022, while digging into the branch’s loan books and interrogating his colleagues, he made mind-blowing assessments.

Since 2015, the whistleblower concluded, more than 10 Toronto-area HSBC branches had issued at least $500-million in home loans to diaspora buyers claiming exaggerated incomes or non-existent jobs in China.

These foreign-income scams spiked during the pandemic, the whistleblower believed, because borrowers could somewhat plausibly claim to be working remotely in other countries while riding out Covid-19 in Canada.

While a small bank of Aurora’s size was expected to issue about $23-million in residential loans every year, this branch had shovelled out $88-million in mortgages in 2020, according to the whistleblower, and over $50-million in 2021.

The whistleblower, whomThe Bureau is calling D.M., immigrated to Canada as an international student from India, making him a minority among mostly Chinese-Canadian co-workers at the Aurora branch.

As D.M. probed his colleagues, his belief gained conviction, that HSBC Canada and other Canadian banks including CIBC had systemic problems with highly questionable mortgages issued to diaspora buyers with unverified sources of wealth in China.

Losing sleep, in April 2022, D.M. sent an audacious email to senior bank executives: “I am going to reveal potential mortgage fraud at HSBC Bank Canada and possibly some employees benefited from the fraud, financially pocketing thousands of dollars, which I call the proceeds of crime.”

D.M.’s explosive four-page complaint triggered an internal investigation that led to some reforms at HSBC Canada according to internal emails obtained by The Bureau.

But more than a year later, D.M. was so dissatisfied with the bank’s response that he risked sharing his story and numerous internal documents for an unprecedented journalistic investigation into Canada’s housing affordability crisis.

“I found out a huge mortgage fraud showing borrowers with exaggerated income from one specific country, China, pretending to be working remotely,” D.M. informed The Bureau in June 2023. “I believe the housing prices in Toronto are linked to this, because this is about income verification in banks, which is supposed to moderate demand.”

The Bureau asked HSBC Canada to review emailed information for this story and provide an appropriate manager for an interview regarding D.M. ‘s records and allegations.

“I won’t have anyone to speak with you directly,” Sharon Wilks, Head of Communications, responded. “But for context: As a global bank, HSBC is at the forefront of efforts to identify, prevent and deter financial crime … We will not do business with individuals or entities we believe are engaged in illicit conduct.”

Wilks added that HSBC Canada “can and do regularly exit relationships with clients whose activities we deem too risky.”

The Bureau’s seven-month investigation into D.M.’s allegations suggests HSBC Canada and other Canadian banks could have issued many billions of dollars in questionable mortgages to Chinese diaspora buyers, and a significant cause of Canada’s real estate bubble is hundreds of billions in illicit fund transfers from China into Canada, and bank lending that amplifies its impacts, especially in Toronto and Vancouver home prices.

“There are thousands of these cases, large scale,” D.M. said in an interview. “Hardworking Canadians are denied mortgages and these Chinese residents forge documents and get mortgages approved, heating up the already hot Ontario real estate markets.”

“These people don’t have steady jobs or income in Canada,” he alleged, “but what they are doing is scams to launder money, and get mortgages using fake documents.”

The Bureau’s investigation included asking seven prominent Canadian experts to assess some of D.M.’s documents, allegations and conclusions.

This investigation suggests D.M. ‘s calculation is plausible, that the Aurora branch and other Toronto-area HSBC branches have issued at least $500-million in questionable Chinese income loans since 2015.

But D.M’s findings could also change the public’s understanding of housing affordability in Toronto and Vancouver, a politically explosive issue expected to frame Canada’s upcoming federal election.

This is because, according to the academics and criminologists that reviewed D.M.’s documents with The Bureau, his evidence fits into FINTRAC’s much broader examinations of suspicious real estate and banking transactions.

In 2023, the anti-money laundering watchdog published a ground-breaking study into 48,000 Chinese diaspora banking transactions.

FINTRAC found that during the Covid-19 pandemic, because Canadian casinos were closed, Chinese underground banking schemes evolved, flooding electronic fund transfers from Hong Kong into Canadian bank accounts that served like corridors for murky real estate transactions.

The Bureau’s analysis also finds that what D.M. discovered in Toronto banks, finally sheds light on mysterious capital flows discovered by a prominent Canadian academic in 2015, in a study of Vancouver land titles and mortgages.

That examination of $525-million worth of real estate purchases in a six-month period found 66 percent of buyers in several affluent neighbourhoods were recent Chinese diaspora migrants, and most mortgages went to buyers with little or no income in Canada.

Similarly, what D.M. found in his probe of pandemic-era loans could be called the evolving “Toronto Method” of an underground banking system discovered first in Vancouver, and found to be laundering a stunning $1.2-billion in cash from Mainland China through British Columbia government casinos in 2014.

This system of shadowy transfers was dubbed the “Vancouver Model” by an Australian professor, and brings together transnational organized crime, affluent Chinese nationals seeking to export their wealth abroad, and Canadian casinos, banks and real estate, in transactions that evade policing because the pivotal cash exchanges are done off the books by professional money launderers serving the global Chinese diaspora.

According to FINTRAC’s 2023 study of 48,000 pandemic-era transactions, this evolving Vancouver Model network “simultaneously facilitates money laundering and the circumvention of Chinese currency controls”

“As a result of the temporary closures of Canadian casinos due to the COVID-19 pandemic, professional money launderers began to diversify their money laundering methods,” FINTRAC’s study says.

“During this time, FINTRAC observed a rise in money laundering typologies involving transferring large sums of funds to Canada from foreign money services businesses, often located in China, notably Hong Kong, and the laundering of the funds primarily through the real estate, securities, automotive and legal professions.”

These wire transfers from China were routed into bank accounts of “multiple, unrelated individuals in Canada,” that served as “money mules” in byzantine networks involving Canada-based real estate developers, real estate agents, mortgage brokers and banks.

These Chinese diaspora bank account owners often claimed they were students, homemakers, office managers, or unemployed, FINTRAC reported.

They sometimes used their accounts to send bank drafts to others in Canada for home purchases, or served as “straw buyers” for offshore investors.

“Mortgage payments are sourced from incoming funds from China,” FINTRAC’s alert said.

FINTRAC’s study doesn’t say that Canadian banks knowingly issued fake-income mortgages to Chinese diaspora buyers in Toronto.

But in an interview, D.M. said banking staff are trained to guard against fraud, and the loan application packages he reviewed in Aurora beggared belief.

“The bank found out that one lady works in a casino part-time but got a $1.4 million mortgage showing over $300,000 annual income,” he said. “Plus she takes money as benefits from the government, for her two kids.”

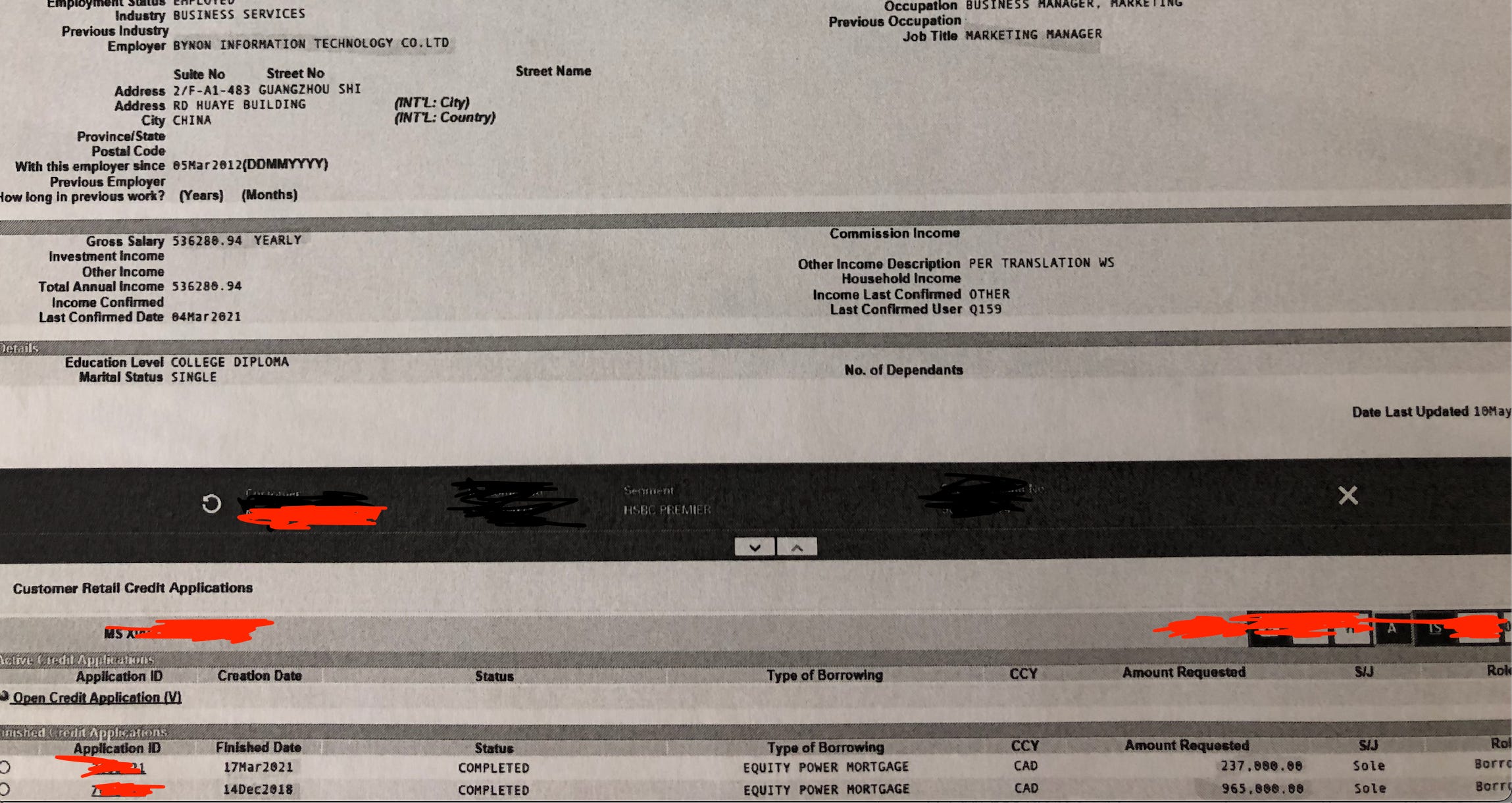

In other examples, an HSBC mortgage client claimed to earn $700,000 annually for remote work in China, while simultaneously living in Canada and paying off a $10,000 student loan.

Another woman who owned homes in Aurora, Markham and Scarborough, worked part-time as a hairdresser while also claiming to earn $536,280 at a “Business Manager” job in Guangzhou.

“Canadian workers have been put out of the real estate market by people working as a hairdresser that own a couple homes,” D.M. said in an interview.

“How is that fair?”

The most shocking case reviewed by The Bureau, shows that one woman that owns at least four Toronto properties opened her HSBC Aurora bank account in 2012, claiming to be a “Homemaker with no annual income.”

But her Toronto account soon received incredible amounts of wire transfers from HSBC China accounts, and paid out “high value cheques” to third parties for real estate purchases.

This case suggests “Toronto Method” shadow banking described in FINTRAC’s 2023 study has been seeping into Toronto real estate for about a decade.

And yet in 2020, this same woman applied for another HSBC Canada mortgage, claiming to earn $763,000 remotely from her job in China.

This evidence from the HSBC whistleblower complements the seminal investigations of Simon Fraser University academic Andy Yan, who examined sales from August 2014 to February 2015 in several communities on Vancouver’s westside. The average home price in Yan’s study was $3-million.

Looking back at his Vancouver findings in comparison to D.M.’s Toronto banking documents, Yan told The Bureau “I think this helps affirm some of my early work that I did, almost nine years ago.”

“This goes to the core of our banking system,” he said, “and how are we verifying identities and how are we verifying incomes.”

In Yan’s controversial study the vast majority of mortgages went to buyers listing their occupation as home-maker, followed by students, and managers. HSBC and CIBC were the dominant lenders.

Unlike the HSBC whistleblower, Yan had no access to internal banking data regarding the purported origin of funds behind these mortgages taken by Chinese diaspora buyers.

But in an interview, Yan said what he found most interesting back in 2015, was suspicions that Chinese migrants were often buying homes with bulk cash, weren’t accurate. The truth was more complex and seems to be clarified by D.M.’s mortgage findings in Toronto.

“It’s about that global flow of capital, and how it’s multiplied by Canada’s mortgage and lending system,” Yan said. “Because you have to remember, one of the biggest conclusions about my study was that it wasn’t bags of cash that were being used to purchase Vancouver homes outright. They were loans being used. So now, I’m thinking, this is where my study connects up to what you have discovered in Toronto.”

“The interesting story here,” Yan added, “is what happens in Toronto real estate may not repeat Vancouver, but it perhaps rhymes.”

Probably the most famous Chinese property owner from Yan’s 2015 study areas is Huawei executive Meng Wanzhou. In 2009 her family bought a home in Vancouver’s Dunbar neighborhood for $2.73 million, land titles show. In 1998, ten years before Vancouver Model transactions started to surge in Vancouver real estate, the home was sold for $370,000. The home is now valued at almost $6-million.

Ashleigh Gonzales, a former RCMP data scientist who recently published a criminology thesis finding Chinese diaspora underground banking causes significantly more money laundering into Canada’s real estate than previously estimated, said that D.M.’s findings resemble her own Vancouver Model research.

“This whistleblower’s allegations of widespread mortgage fraud at HSBC Canada align with some of the first-hand accounts from staff of some Canadian financial institutions that I have come across in my research on money laundering in British Columbia,” Gonzales said.

Gonzales, who worked for RCMP’s anti-gang unit in British Columbia until 2023, says she found reports of mortgage fraud accelerated “during the uptick in the Canadian housing bubble after the Vancouver 2010 Olympics,” and continued to surge from 2015 to 2018.

With all this considered, and comparing data sources in this story with previous evidence confirmed in British Columbia’s Cullen Commission, The Bureau estimates that from 2014 to 2023, well over $200-Billion in Vancouver Model and Toronto Method funds could have poured through underground diaspora networks and Canadian financial institutions into Toronto and Vancouver’s real estate.

A federal official not authorized to comment publicly also examined D.M.’s banking leaks for The Bureau, and called this information “explosive.”

The official said money laundering is increasing in Canada, and D.M.’s belief that Chinese-income mortgage fraud has boosted home prices in Toronto is likely true, but also should apply for Vancouver and Montreal real estate prices. The official noted that other nations require tax agencies to verify incomes for mortgages, which isn’t the case in Canada.

“It matters for our next generation because of the impact on the housing market,” the official said.

Queen’s University professor Christian Leuprecht – editor of Dirty Money, a new academic text that probes how Ottawa’s weak regulation has “turned the Canadian federation into a destination of choice for global financial crime” – also reviewed some of D.M. ‘s leaks.

“It’s not a new problem, but you’re taking it to the next level,” Leuprecht said.

“Why does this matter? Because organized crime isn’t just laundering their ill-gotten gains, like any good business person, when they buy real estate, they generate a down payment, then get a mortgage for the rest. Why buy one property when you can buy four?”

The Bureau’s review of HSBC Canada emails and D.M.’s text messages, shows he came to believe numerous employees at the Aurora branch had direct knowledge of faked Chinese income mortgages, and a veteran manager with oversight of more than 10 Greater Toronto branches knew about broad and questionable mortgage lending for Chinese diaspora clients.

Months after D.M. blew the whistle internally he exchanged texts with another employee, identifying colleagues that they believed had knowledge of diaspora mortgage scams.

The texts suggest D.M. believed HSBC Canada and other Canadian banks continued to hold vast amounts of suspicious foreign income mortgages, which could cause systemic loan quality risks if Toronto’s real estate prices decline.

“Do you know how many mortgage frauds we have in our books,” D.M. texted to his colleague. “It’s insane.”

“She told me,” the colleague replied, referring to an HSBC branch manager.

“She was like, if you do come, you gotta be prepared for the mortgage payout.”

“These people showed fake income and got mortgage,” D.M. continued. “Now interest rate is high, they can’t cope.”

“Other branches did the same thing too,” his co-worker replied. “I heard there’s a lot.”

“Absolutely,” D.M. texted. “All branches engaged in it.”

“This is like the unspoken secret,” his co-worker concluded. “I’m pretty sure other banks have it too. My Aunt have no income and got a mortgage for 700k. They just need a Covenanter from China.”

Generally, in mortgage contracts a covenanter takes responsibility for the loan if the primary borrower defaults.

Internal records reviewed by The Bureau confirm that on April 18, 2022, D.M. sent a lengthy complaint email to senior HSBC Canada executives, informing them of allegations he’d learned from his colleagues.

In it, he alleges that an Aurora manager had informed him of a complaint letter posted to the branch, that accused mortgage brokers and branch employees of colluding in scam mortgages emanating from Mainland China fraud networks.

Pointing to specific examples, D.M. claimed that another branch colleague had admitted processing numerous loan applications without meeting his clients, because a branch manager delivered her subordinates foreign income client applications so “they did not have to get sales themselves.”

“Surprisingly all these clients he would get will have foreign income most of the time very inflated like 400k or 670k a year,” D.M. wrote. “To me that’s suspicious, but he never questioned the branch manager because in Asian culture it’s disrespectful to question elders.”

D.M. also informs his bosses that one Aurora bank manager opened up to him, saying she believed allegations of mortgage fraud collusion involving some branch staff.

“She said yes, she knows specially in Mainland China there is a team who would even answer emails and phone calls verifying [Chinese income] but it’s a sophisticated and well organised scam,” D.M. ‘s email to HSBC Canada managers says.

His complaint explains that he continued to press an Aurora bank manager on her knowledge of fraud allegations.

“When I asked for such a serious issue if she raised a HSBC confidential [complaint] or not she evaded my question,” D.M. wrote. “Now we all love numbers, but I don’t think the bank will like these kinds of numbers achieved through this way.”

Describing why he contacted HSBC Canada executives directly, the whistleblower’s complaint says he felt confused and isolated, but D.M. decided “local leadership if not participated, at least turned a blind eye,” to Chinese fake-income scams, forcing D.M. to “bring up a serious issue against people of superior positions.”

“I could not have stayed silent, in fact I could not sleep well thinking about it,” his April 2022 complaint says. “It reminds me to some extent what happened with the Home Capital Group.”

“The whole thing is wrong on so many grounds,” D.M. continued.

“Now I know one more reason why Canadians and permanent residents are not getting into the housing market. It’s not only HSBC such things are happening across other Canadian banks as well.”

In the Home Capital case, the Ontario Securities Commission fined the prominent Ontario-based subprime mortgage lender in 2017, alleging Home Capital failed to disclose several of its mortgage brokerages had major problems with faked-income mortgages.

D.M. concluded his four-page complaint to senior executives, writing: “I recommend all mortgage deals of this branch in the last 3 years at least if not longer with Foreign income be probed.”

“Bank statements can be verified directly with the foreign banks or use a reputable third party to verify,” he suggested. “When we find someone with Fake ID or trying to impersonate someone we call the cops. But these people, both staff nor clients who did fraud were reported.”

Hours later on April 18, 2022, an HSBC Canada executive emailed back: “I am going to refer this to our Fraud and Risk teams and they will investigate your concerns.”

The next day D.M. continued to hound HSBC Canada managers with emails to support his allegations, spotlighting the absurdity of massive Chinese remote incomes claimed by diaspora buyers.

He pointed to one woman with a $1.6-million HSBC Canada mortgage.

“The client claims to be in Canada but [is] a office supervisor in China. [In the] age of remote working in which country [does] a office supervisor makes 400k please tell me,” D.M. wrote.

“[W]hen I asked the co-worker she said her job is not to use the brain or be a police, when I asked do you think she makes that kind of money and how is she doing her job being in Canada to be an office supervisor in China[?]”

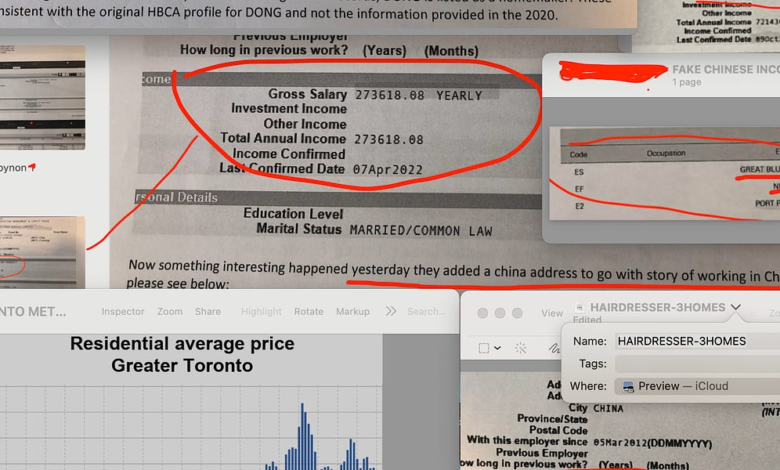

Pointing to another document, D.M. warned his managers about Ms. Chen, who claimed to make $721,000 annually as “project manager” for a Beijing telecommunications company, to secure a $1.89 million mortgage.

Again on May 4, 2022, D.M. emailed executives, suggesting internal records for an Aurora client named Ms. Jin had been altered soon after D.M. blew the whistle on fake Chinese income loans.

His email, which included Ms. Jin’s client profile, warned: “Something interesting happened yesterday, they added a China address to go with [the] story of working in China, please see below.”

The Aurora branch banking records disclosed to The Bureau show that Ms. Jin owns three homes in the blocks surrounding Pacific Mall in Markham.

“The client was onboarded on 24th March with Canada address only and Canadian tax residency,” D.M.’ s email continued.

“She claims to be working in China and have foreign income, so the story she is stuck in Canada due to Covid is very interesting. Suddenly yesterday she decided her address in China. Someone saw the discrepancies and the branch team decided to change it.”

“To me that’s a red flag done to align with the story portrayed.”

Next, D.M. exposed Ms. Chen’s foreign income claim.

“She works for Food processing company, a logistics officer making 273k a year,” he wrote. “I don’t know which logistics officer can work when physically in a different company and also who makes 273k working as a logistics officer.”

Citing another internal banking record, D.M.’s email pointed to Ms. Jin’s $273,000 income and said “it’s interesting how they did the verification.”

The email continues to explain that branch records showed Ms. Jin and her husband had a joint mortgage with a balance of $497,000 at CIBC.

But suddenly during Covid-19, Ms. Jin applied for a new mortgage for $1.2 million with HSBC Canada.

“When I see such things I can’t stay quiet,” D.M.’s May 2022 email says. “[I] was assuming with the new rules things will stop, [but] declining the mortgage or retraining the staff is like treating the symptoms.”

He added that many suspicious Chinese income loans had been “flagged by our Fraud Team already.”

The whistleblower’s scathing assessment ends with the observation that D.M. didn’t believe “someone woke up and decided to scam the bank, but [worked with] a sophisticated network of agents who are training people what to say and answer.”

“The implications are broader and as a responsible bank and citizen we have to,” request investigations from the Canadian Revenue Agency or Ontario Provincial Police, D.M. asserted.

The Bureau asked Ashleigh Gonzales, the former RCMP data scientist, to review some of D.M.’s documents and conclusions.

“From what I have reviewed, D.M.’s findings align with what appear to have been commonplace practices by some groups of staff complicit from the front line, middle office, and back office and sanctioned by management,” Gonzales wrote, adding “whether knowingly or not depends on the individual work cultures.”

The Bureau also asked Stephen Punwasi to review D.M. ‘s leaked banking documentation.

Punwasi is a financial expert who founded Better Dwelling, a real estate analysis website with a large following of young professionals trying to understand why they’re excluded from home ownership in Canadian cities.

He also provided analysis for British Columbia’s 2018 report into Vancouver Model money laundering in casinos, real estate and luxury vehicles.

What Punwasi explained to the report’s author, former RCMP executive Peter German, is that even though Vancouver Model money launderers don’t comprise a majority of buyers in Vancouver, their willingness to overbid on home sales causes ripples that sends prices skyrocketing, especially during times when political turmoil inside China triggers increased capital flight.

“In 2015 and 2016 Ontario saw this flood of money from China, just like British Columbia, and it was not just to do with immigration, it was due to President Xi’s political crack down on corruption,” Punwasi said. “I think we’ve seen that capital flight in Ontario and B.C. in two big cycles, also including 2020 and 2021.”

The Bureau asked Punwasi if the banking records disclosed by D.M. help to explain Toronto’s real estate price surges.

“Absolutely,” he said, pointing to the case of Ms. Jin (who claimed a $273,000 remote-work income in China) and her three homes surrounding Markham’s Pacific Mall.

Property buyers that aren’t shopping for shelter, but for capital flight or money laundering vehicles, are what Punwasi terms the “marginal buyer.”

“The marginal buyer is like an exuberant buyer on crack, so if they are motivated to move as much money as possible,” he said, “the larger the mortgage they can get, it helps them to overpay for homes, and that can cause the price to launch.”

“So if you see a townhome in Toronto going for $2-million, you don’t know if it is mortgage money laundering or someone buying a place to live. You just have to compete with the going price.”

Punwasi says housing prices are a powerful political issue that will shape the next federal election.

But at the same time, young generations are confused by competing explanations on the causes of Canada’s housing affordability crisis, Punwasi believes, whether its lack of housing supply due to restrictive zoning bylaws, or increased demand due to recent immigration surges, or other factors that make Canada’s housing bubble an outlier in the Western world.

“There are so many conflicting narratives right now that people find it hard to believe the scale of impact that money laundering can have on Toronto real estate prices,” Punwasi said. “But no one has thought it through, that having criminals run our renting stock is a liability.”

Punwasi also believes that Prime Minister Justin Trudeau’s government has decreased scrutiny of money laundering in recent years.

He points to new data uncovered in a ministerial inquiry from Conservative MP Adam Chambers, who is a proponent of tougher money laundering laws, which found sharp declines in Canadian Revenue Agency audits of FINTRAC leads.

“The systemic corruption in housing has been snowballing,” Punwasi said, “to where it’s turned into, maybe the banks don’t need to check where the incomes are coming from, and now whole generations can’t find stable shelter.”

HSBC Canada emails reviewed by The Bureau show that while the bank appears to have responded to some of H.M. ‘s recommendations in 2022, troubling mortgage applications and problems with existing Chinese income loans continued.

A January 2023 email to an Aurora branch manager from HSBC Canada’s office in Montreal pointed to a client named Ms. B., who worked at an Ontario government casino, and owned homes across Toronto, in Richmond Hill, Newmarket and East York.

Documents show she obtained an HSBC Canada mortgage for $1.26 million in 2016, and that HSBC Canada staff “confirmed” in July 2021 that she was earning $345,000 with a remote work job in Beijing.

Despite her incredible claimed income, documents show, Ms. B. was having trouble paying at least one of her three mortgages.

An email from a “Senior Loss Mitigation” employee in Montreal to an Aurora branch employee says: “client is going through a tough time … her income is limited … I know she collect rent and she use it to pay her second mortgage. Please review the situation with the client to see if there is any special agreement available to her.”

But Aurora’s branch wrote back to the Montreal branch: “What we have told her is … if she really can’t pay, then she just have to put her house for sale … but she doesn’t want to do that.”

In an interview D.M. told The Bureau this case was typical.

“What they are doing is AirBnBing these properties,” he said. “But they can’t manage with higher interest rates.”

He said during mortgage application interviews at the Aurora branch he would often look across his desk and ask questions without letting clients know he was looking at their income claims from purported Chinese companies on his computer screen.

“Most of these people don’t even know what type of company is in their job profile,” he said.

And documents reviewed by The Bureau show that mortgage applications consistent with Fintrac’s 2023 Chinese money laundering report continued in Aurora.

In May 2023, D.M. emailed a senior HSBC Financial Crime Compliance investigator, writing “Just came across two profiles of clients and I have strong evidence these mortgages were also obtained with fake docs and fraudulently.”

When the investigator responded “I will take a look,” D.M. replied: “One had a CDA student loan of 10k and making 700k in China. Makes no sense, there are many other anomalies.”

In interviews, D.M. told The Bureau he waited “patiently for a year” after reporting his Chinese-income mortgage concerns to HSBC Canada managers, before concluding the bank’s response was insufficient.

“This has been going on for seven years and no one spoke up,” he said. “In my first meeting last year, they asked me a lot of questions, like why didn’t you use the normal channels? But I had no faith in the normal channels.”

“Many bank staff were obviously involved,” D.M. alleged. “It was not one or two employees turning the blind eye but the entire system, someone verifying those fake offer letters and pay stubs, or their bank statements from China.”

D.M. said his concerns also included HSBC Canada’s proposed sale to RBC, which was announced in 2022, about six months after D.M. ‘s April 2022 internal complaint. The sale was approved in December 2023 by Canada’s deputy Prime Minister Chrystia Freeland.

Christian Leuprecht, among other experts interviewed for this story, agreed that D.M.’s allegations of widespread Chinese-income frauds at HSBC Canada could raise questions about whether Freeland, Canada’s finance minister, had knowledge of mortgage lending investigations inside HSBC when she approved the sale.

Freeland directed RBC to “establish a new Global Banking Hub in Vancouver,” and “maintain Mandarin and Cantonese banking services at HSBC branch locations,” a Department of Finance statement says.

Ultimately, D.M. says he chose to share his story with Canadian citizens partly because he felt pressured to erase evidence from his whistleblower complaint emails.

A June 2023 email from the bank’s personnel department says “we hereby demand that you immediately and permanently delete any and all HSBC information on any personal email accounts.”

“If you do not comply with these obligations,” the email warns, “HSBC also reserves the right to bring this matter to the attention of relevant law enforcement agencies.”

Another July 2023 email from senior management said: “I will reiterate how much we appreciate that you spoke up,” and confirmed that D.M.’s complaints to HSBC Canada resulted in “several enhancements to income verification procedures.”

The manager’s email continues, saying “as part of your escalation, you sent confidential information from the bank to your personal email account,” and asserts that D.M. had promised to delete the “confidential client information in your personal possession.”

“I could not sleep, and they were telling me delete, delete, delete,” D.M. recalled in an interview.

HSBC Canada did not respond to follow-up questions from The Bureau regarding D.M.’s specific allegations.

Now he is looking for accountability.

“There should be a thorough, retrospective audit of HSBC Bank mortgage deals and eventually all Canadian banks in Canada and stricter regulations when it comes to mortgage approval showing foreign income,” D.M. said, “because there are many skeletons in the cupboard.”

Garry Clement, a former RCMP anti-money laundering expert who also contributed to the Canadian academic text Dirty Money, reviewed some of D.M.’s Toronto Method documents, and commented “the best description of the bank’s actions, is willful blindness.”

“This is one well-documented example of how banks are catering to Chinese citizens without following strict know your customer guidelines as they would for any Canadian,” Clement said.

“We must recognize that a lot of the loans occurred at a time when our political leaders catered to China with a naïve understanding.”

Calvin Chrustie, a former RCMP transnational crime investigator whose recent report finds Canada’s weak regulations have made the nation a playground for underground banking linked to organized crime in China, Iran and Mexico, noted that in 2012, U.S. regulators hit HSBC with a $1.9 billion fine because of $881-million in suspicious transactions with Mexico’s Sinaloa cartel and Colombia’s Norte del Valle cartel.

“The bigger question in Canada now is why aren’t we looking at what is happening in the banks?” Chrustie said. “We haven’t looked at the complicit actions of financial institutions, while we rely on well-intended entities like FINTRAC, who like police are often restricted in what they can do, or say to the public.”

FINTRAC would not confirm or deny whether its recent fines on CIBC for failing to report suspicious wire transactions and a fine on RBC for failing to report suspicious transactions related to frauds, relate to FINTRAC’s 2023 report on Chinese shadow banking and pandemic-era bank account and real estate transactions.

FINTRAC also would not confirm whether a Globe and Mail report that TD Bank faces a money laundering compliance fine of more than $10-million is accurate, or relates to the Covid-19 shadow banking schemes.

Like the former RCMP experts interviewed for this story, Andy Yan says governments in Ottawa and British Columbia and Ontario are ultimately responsible for ushering mysterious wealth into Canada’s homes.

“It’s like, this isn’t entirely new, what you have found in Toronto,” Yan summed up.

“When you have programs that are directly meant to domesticate foreign capital into local real estate markets, you start seeing these patterns or these incongruities between incomes and house values. And we have institutions that really are supposed to safeguard us in terms of transparency and accountability.”

Meanwhile, a second property owned by Meng Wanzhou in Vancouver attests to the murkiness surrounding Chinese wealth, but also broader concerns of former RCMP experts interviewed for this story, on how and why Chinese state and non-state actors move funds globally.

In 2016 Meng, who held at least seven different visas or passports, purchased a $15-million mansion with an HSBC Canada mortgage in Shaughnessy, a luxurious community just outside of Yan’s study areas.

Other mansions in Shaughnessy featured prominently in a confidential RCMP study of all homes sold for between $3-million and $30-million in 2016. That police intelligence study found Chinese transnational gangsters and Vancouver Model suspects linked to over $1-Billion in property purchases in 2016.

Ironically — in the case that disrupted Canada’s warming relations with China under Justin Trudeau — Meng finally admitted to U.S. government financial fraud charges that she misled HSBC about international transactions, and “Meng and her fellow Huawei employees engaged in a concerted effort to deceive global financial institutions, the U.S. government and the public about Huawei’s activities in Iran.”